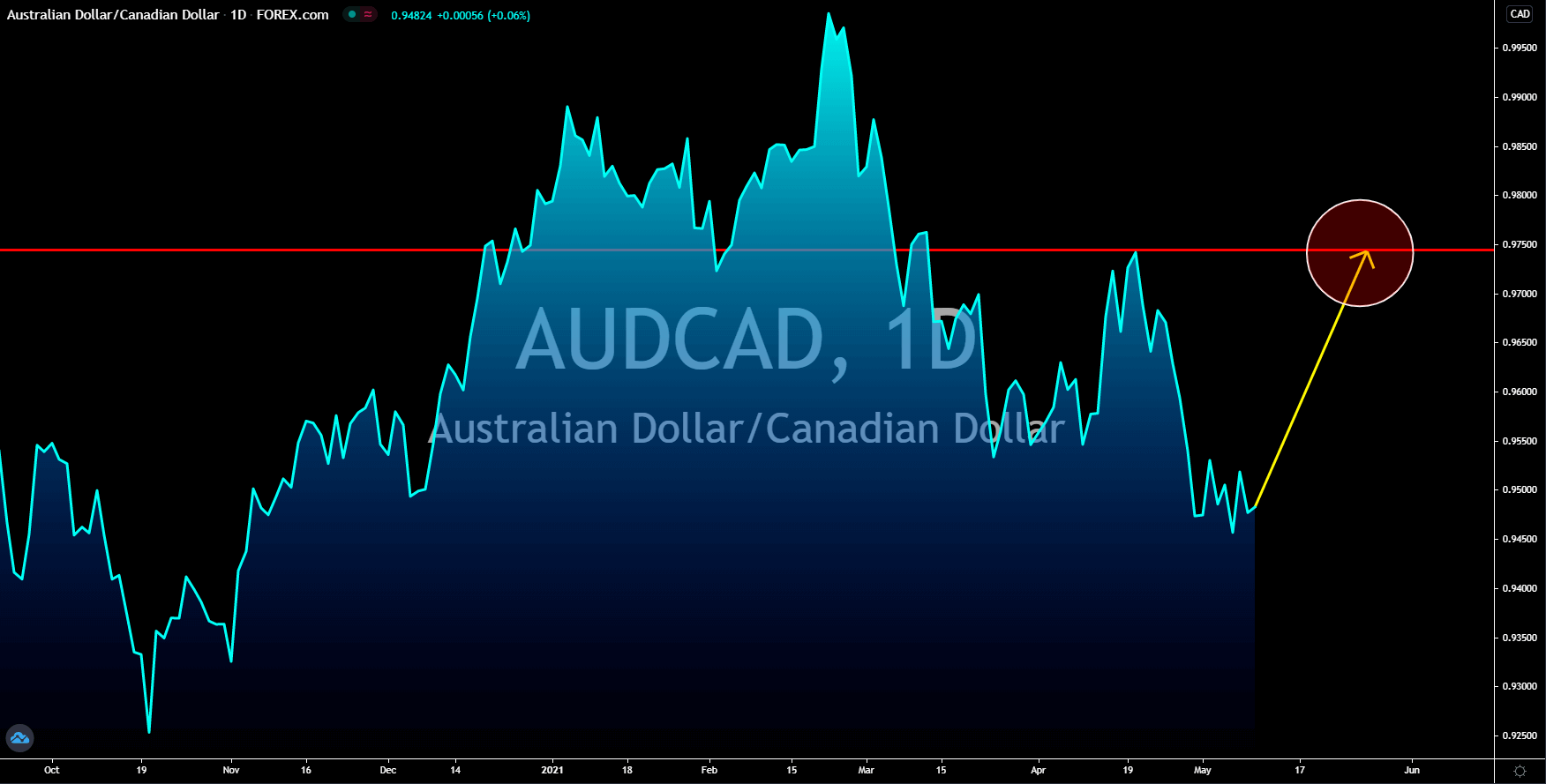

AUDCAD

The Australian dollar will recoup its losses against the loonie after Canada published disappointing results for the labor market. Unemployment in the country rose by 0.6 percentage points to 8.1% in April with worse-than-feared job loss of 207,100. On the same day, the US tallied 266,000 jobs added, which was a major missed from the 978,000 estimates. Around 6.1% of the US workforce were unemployed, up from 6.0% in March. The same weak performance can be seen on Canada’s seasonally adjusted Ivey PMI, which dropped to 60.5 points from 72.9 points in the prior month. Despite this, analysts are optimistic that Ottawa will return to its pre-pandemic level at the second half of fiscal 2021. During the March preliminary report, Canada expanded by 0.9%, which could be the 11th consecutive month of GDP advances if actual result stays on the positive territory. A possible catalyst for the continued momentum in CAD was an interest rate hike from the BOC.

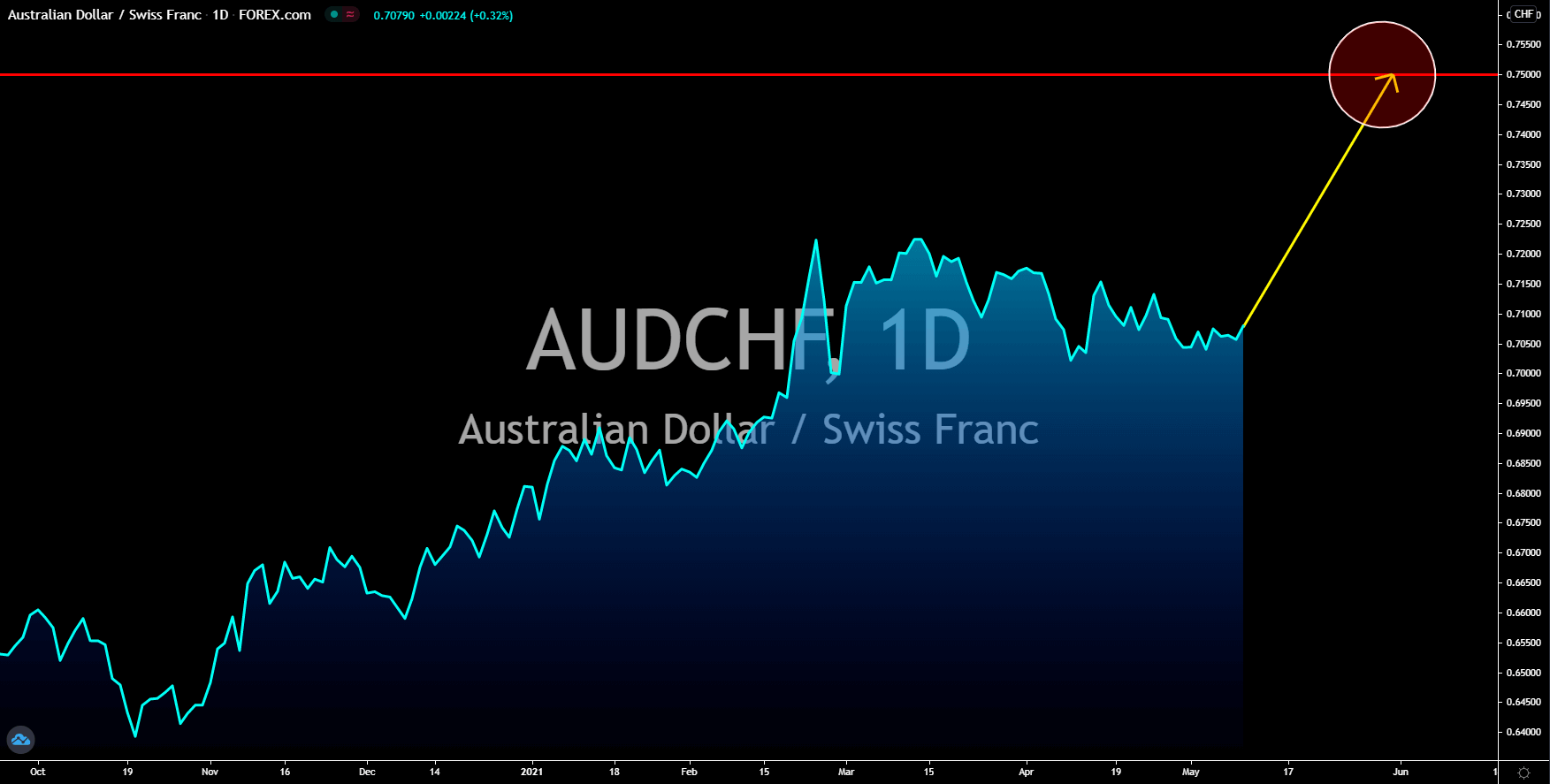

AUDCHF

Unemployment in Switzerland fell for both seasonally and not seasonally adjusted reports. Figures came in at 3.3% n.s.a in April, which topped consensus estimate, and 3.1% for seasonally adjusted result. These numbers were higher from their prior results of 3.4% and 3.3%, respectively. The bettering economic data from Switzerland will boost the local market as the franc plummets against the Australian dollar. In other news, a recent poll conducted by GFS Bern in Switzerland suggests that 49% of the 2,000 voters surveyed will back a Swiss-EU free trade agreement (FTA). Around 15% said they are strongly in favor of the deal while 13% were fully against it. Despite being surrounded by EU member states, Switzerland remains neutral. However, its membership with the European Free Trade Agreement (EFTA) allows it to access the single market. AUDCHF will retest its previous high around the 0.72000 price level before reaching the 0.75000 target area.

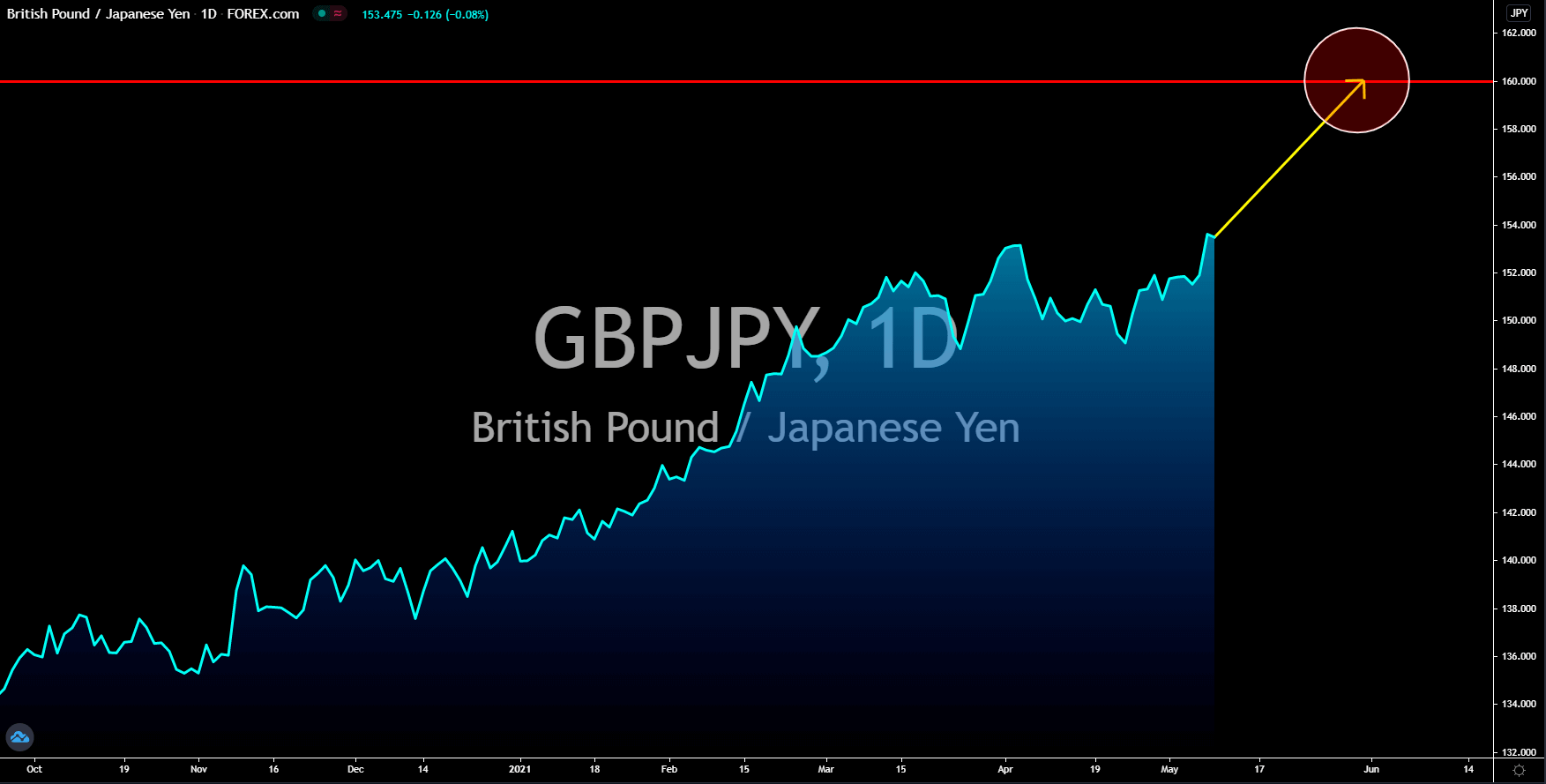

GBPJPY

The long-term economic outlook for the United Kingdom is positive. The Office for National Statistics (ONS) said it is expecting the March GDP data to expand by 1.4% with a Q1 figure anticipated to post better-than-feared. Meanwhile, the Q2 is expected to return in the positive territory at 5.0% as the gradual reopening of the UK economy in mid-March will push GDP higher. As for the full-year projection, the BOE sees surging up to 7.25%, which would erase the losses Britain suffered in 2020. If the actual result came close to projections, it will be the biggest annual GDP increase in the UK since WW2. Goldman Sachs has already hinted that the UK economy will outperform the US this year with 7.8% growth, up from the previous reading of 7.1%. However, the impact of COVID-19 and the UK’s EU withdrawal in January 2021 is expected to slow down the growth, which could impact Britain’s near to long-term economic outlook.

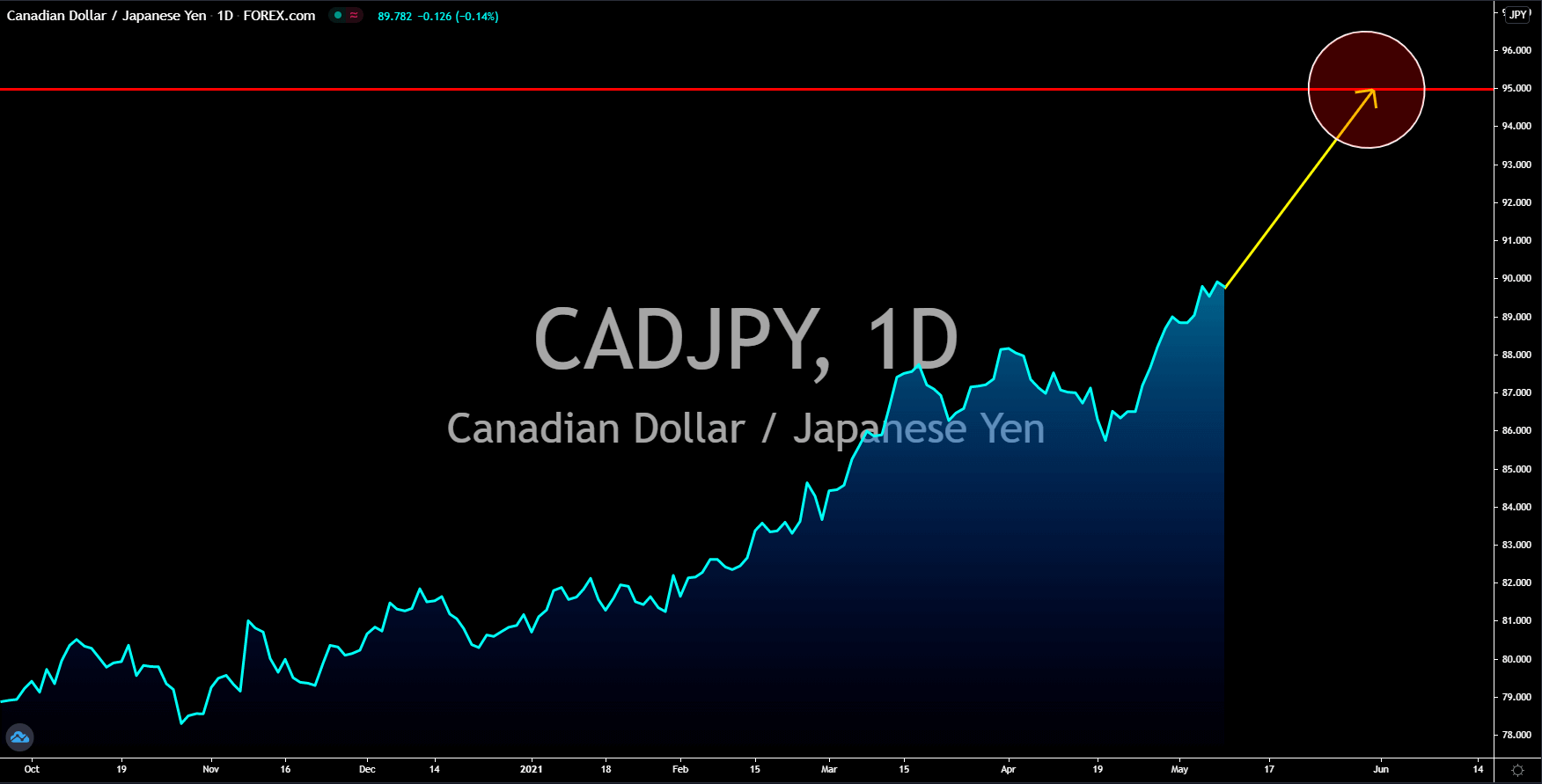

CADJPY

The dovish comments from the Bank of Japan along with bettering economic data from Tokyo will send the yen lower against its Canadian counterpart. Household spending in March soared 7.2%, which was the third-largest percentage increase in record for the report. On a year-over-year basis, this translates to 6.2% jump from -6.6% in February. However, the BOJ said that a continued support by the central bank is needed for the uneven and uncertain economic growth. The Bank of Japan said that while the spending has picked up, it is still far from the 2.0% inflation target it is expecting. BOJ Governor Haruhiko Kuroda expects the central bank to achieve a 1.0% inflation figure by 2023 after decades of low interest rate and massive quantitative easing (QE) program. Meanwhile, Japan is still dealing with the surge of COVID-19 cases, which is now at the fourth wave and is threatening the cancellation of the much-delayed Tokyo Olympics in July 2021.